Marketplace Pulse: Differences in Cost-Sharing Create Barriers to Mental Healthcare in Medicare Advantage

The Marketplace Pulse series provides expert insights on timely policy topics related to the health insurance marketplaces. The series, authored by RWJF Senior Policy Adviser Katherine Hempstead, analyzes changes in the individual market; shifting carrier trends; nationwide insurance data; and more to help states, researchers, and policymakers better understand the pulse of the marketplace.

With the growing popularity of Medicare Advantage (MA) plans has come increased criticism from policymakers and advocates. There has been a longstanding critique about whether insurers use the risk adjustment system to overpay themselves, reflected in a recent report from the Medicare Payment Advisory Commission (MedPAC), which projected that the combined effects of coding intensity and favorable selection will lead the government to spend $88 billion more on Medicare Advantage in 2024 than they would in traditional Medicare. The payment incentives that shape the growth and design of MA plans have important implications for racial equity among Medicare beneficiaries, since Black and Latino beneficiaries are disproportionately likely to enroll in Medicare Advantage, and have been shown to have less access to high-quality plans.

Regulators are more actively scrutinizing communications with consumers, rejecting some advertisements for being misleading, and changing rules about how brokers are compensated. There has also been a rising chorus of concern about how MA plans manage utilization. Some of it has centered on prior authorization and denials. An explosive series of recent reporting focused on Optum's strict adherence to a model that dictated the length of time spent in post-acute care. Former employees reported that required compliance with an algorithm required them to make uncomfortable tradeoffs between patient care and their own performance ratings. Other investigations have found that many services are summarily denied, even if they would be approved in traditional Medicare. When patients appeal, they are likely to win. Provider networks in MA plans have also been criticized for being overly narrow and for containing non-existent providers.

An important focus of complaints about Medicare Advantage concerns access to behavioral health services. This is part of a general concern throughout the healthcare system that access to mental healthcare is inadequate. Recently, the Biden Administration released a proposed rule to make it more difficult for plans to evade their responsibility under the Mental Health Parity and Addiction Equity Act of 2008. However, Medicare is not subject to the Parity Act, meaning that some of the constraints that bind Medicaid, employer insurance, and the individual market do not apply to Medicare Advantage plans.

One issue is a shortage of behavioral health providers who are willing to see Medicare enrollees, leading to the recent change to allow marriage and family therapists and mental health counselors to participate in Medicare. This may have a disproportionate impact on communities of color, who are more likely to be enrolled in plans with lower quality ratings and potentially more narrow networks. For MA enrollees, this provider shortage can be compounded by narrow provider networks. A recent study found that psychiatrist networks in MA plans were narrower than in Medicaid and individual market plans. Congress and the Administration are considering additional measures to increase network adequacy.

Policymakers seeking to increase access to mental health services may also wish to consider patient cost-sharing, which is another component of plan design that can impact access to care. Previously we have reported on cost-sharing in the individual market, where mental health visits often cost patients more than primary care visits. In fact, we found that nearly 20% of silver plans in 2024 had higher copays for a mental health visit.

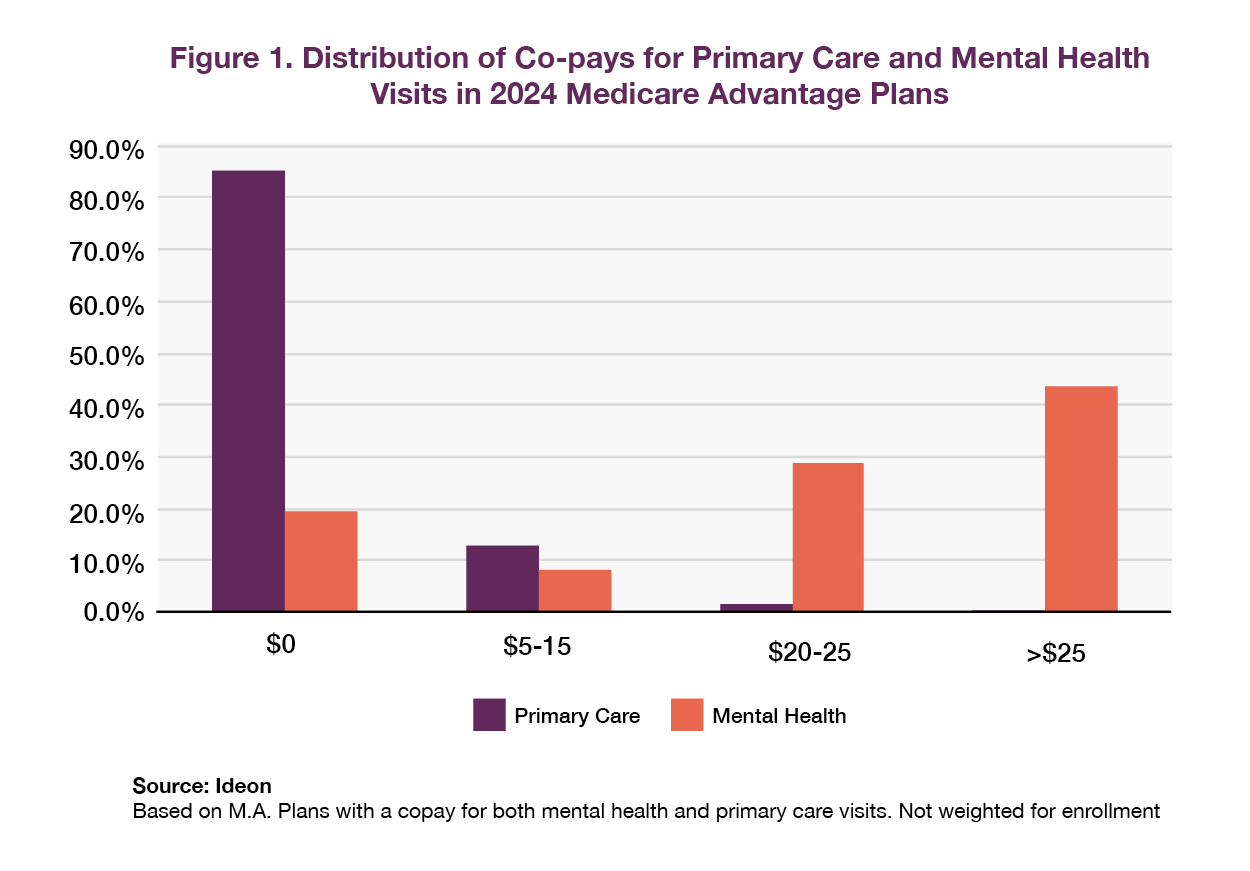

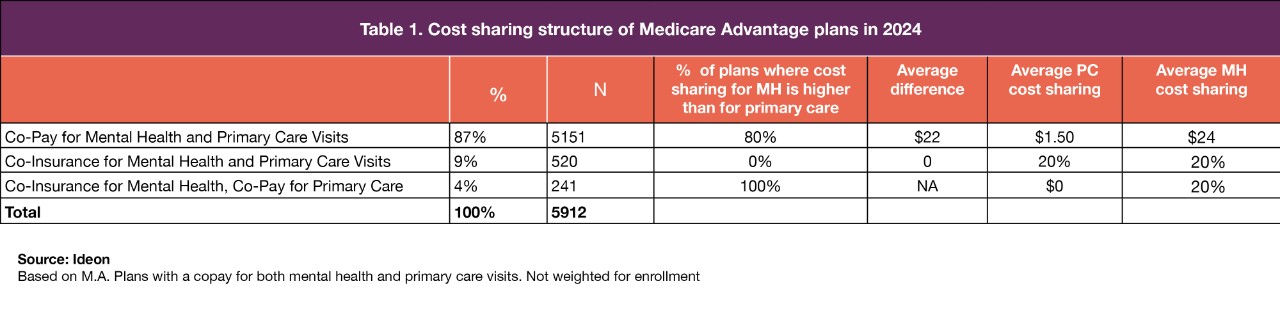

In the case of Medicare Advantage, these differences in copays are far greater. Using data from Ideon, we analyzed nearly 6,000 MA plans on the market in 2024. Higher coinsurance for mental health visits in Medicare was eliminated in 2008, but nearly 90% of MA plans require copays for both mental health and primary care visits. In 80% of these plans, the copay for mental health visits is higher than the copay for a primary care visit. The differences are substantial. More than half of the time, the mental health copay is at least $25 more than the primary care copay, and in 20% of plans, the difference is $35 or more.

Low copays for mental health are a rarity in Medicare Advantage. While the copay for primary care visits was zero in 85% of plans, this is only true for mental health visits in 19% of plans. In three-quarters of plans, the copay for mental health services was $20 or more, which was the case for primary care visits in less than 1% of plans.

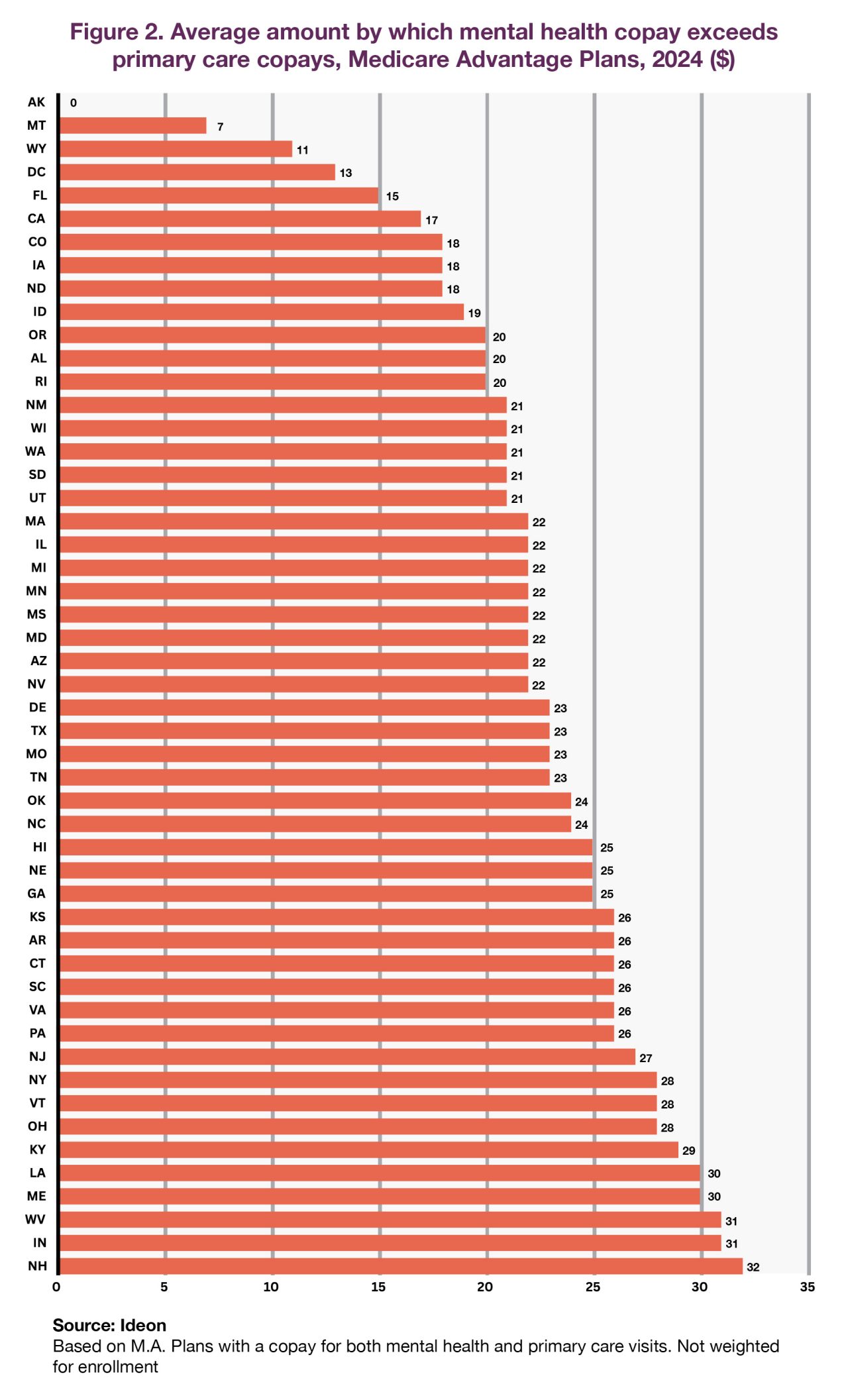

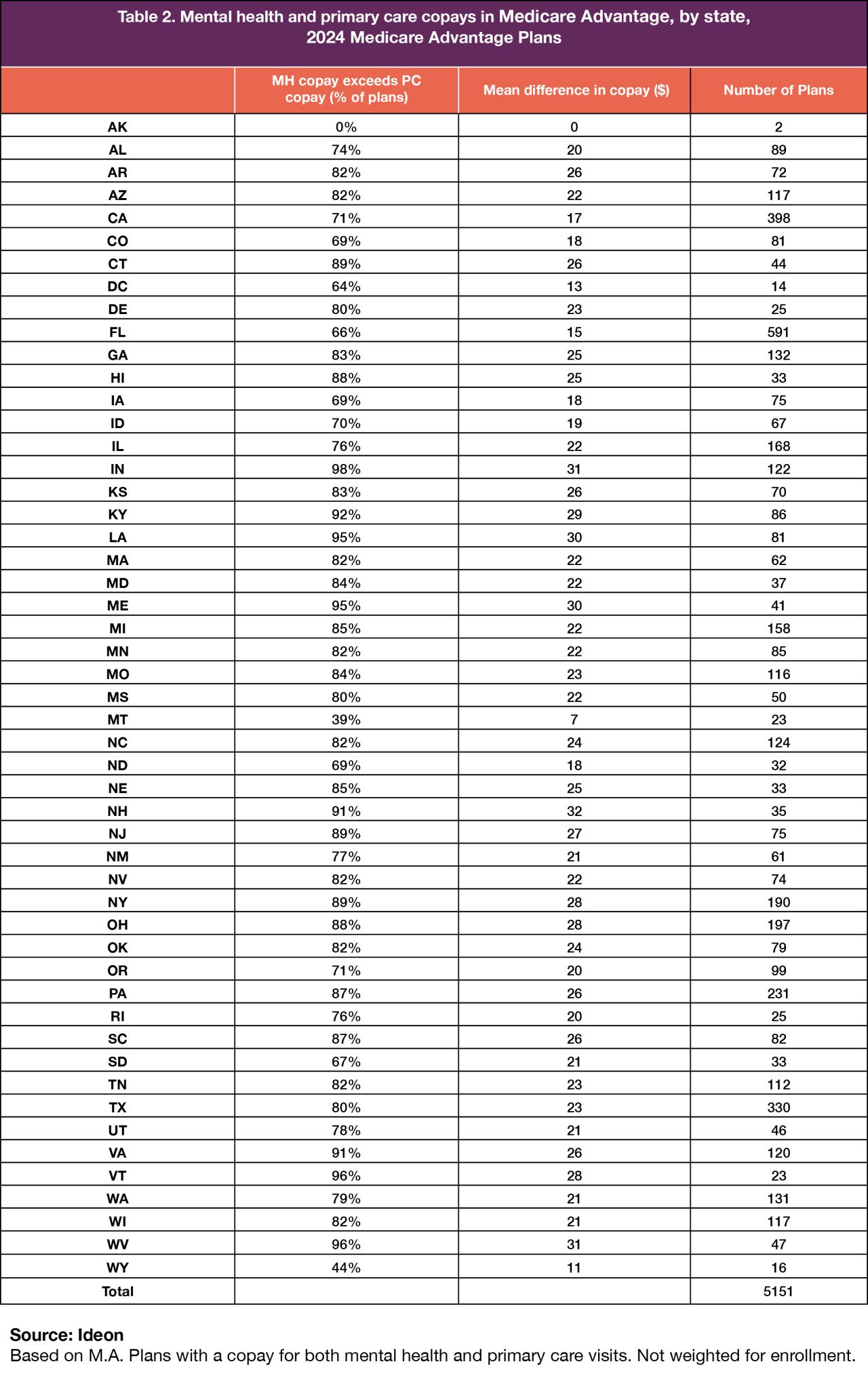

This general pattern of differential cost-sharing is pervasive and shows relatively little geographical pattern, although the average difference between mental health and primary care copays varies somewhat among states.

Scrutiny of MA plans has accelerated, and sustained attention from Congress and CMS should be expected. Additionally, the Office of the Inspector General will be continuing its oversight of managed care as outlined in their recently-released strategic plan. They may wish to include a consideration of differential cost-sharing as part of their analysis of plan benefit design.

Mental Health Support

SAMHSA National Helpline

If you are seeking support for mental health or substance abuse disorders, call the Substance Abuse and Mental Health Services Administration's (SAMHSA) National Helpline at 1-800-662-HELP (4357).

988 Suicide and Crisis Lifeline

If you or someone you know is in crisis, reach the 988 Suicide and Crisis Lifeline by calling or texting 988 or chat at 988lifeline.org.

Related Content

Marketplace Pulse

Marketplace Pulse: The Challenge of Obtaining Mental Healthcare in the Marketplace