Marketplace Pulse: Health Insurance Coverage in Farm Country

The Marketplace Pulse series provides expert insights on timely policy topics related to the health insurance marketplaces. The series, authored by RWJF Senior Policy Adviser Katherine Hempstead, analyzes changes in the individual market; shifting carrier trends; nationwide insurance data; and more to help states, researchers, and policymakers better understand the pulse of the marketplace.

Health Insurance Coverage in Farm Country

Major takeaways:

- The Health Insurance Marketplace (Marketplace) and Medicaid are important sources of coverage in farm states, with between one-fifth and one-third of the states’ populations enrolled in one of these two programs.

- Nearly all enrollees in the Marketplace qualified for Advanced Premium Tax Credits (APTCs), which reduced premiums by an average of $506/month.

- In congressional districts in farm states, combined enrollment in the Marketplace and Medicaid ranged from 14% to 51% of the total population.

- Farm states have seen meaningful reductions in their uninsurance rates since 2014, with an average decline of about 25%.

- Many farmers stand to lose some or all of their tax credits if they are not renewed for 2026.

Nationally, there are about 3.4 million farmers and 2 million farms, the great majority of which (85%) are run by families. Products from these farms contribute to a mammoth agriculture and food supply chain, which according to some estimates supports 24 million jobs and $9.6 trillion in annual economic activity. And while there are farms in every state, the farm population is geographically concentrated. "Farm country" has no exact definition, but it is a way to describe a part of the country where farming is particularly important. Here we focus on the 10 states where farmers make up the greatest share of the labor force: Idaho, Iowa, Kansas, Kentucky, Montana, Nebraska, North Dakota, Oklahoma, South Dakota, and Wyoming. Even in these states, most residents are not farmers, but about 40% of the population is rural—about twice as high as the national average.

Farming is a uniquely challenging occupation that involves a lot of exposure to risk, and access to health insurance is critical. Just as farmers need insurance on their crops and their property, health insurance is also essential. Going without coverage is a major business risk, and unpaid bills resulting from serious illness or injury can lead to the loss of a family farm. Since the population of farmers is older than most workers, the risk of health problems is greater. Further, since most farmers are self-employed, obtaining affordable health insurance has historically been a challenge. The need for health insurance sometimes leads a family member to take an off-farm job just for the benefits, but this strategy limits the growth of family farms and deters the younger generation from entering the business.

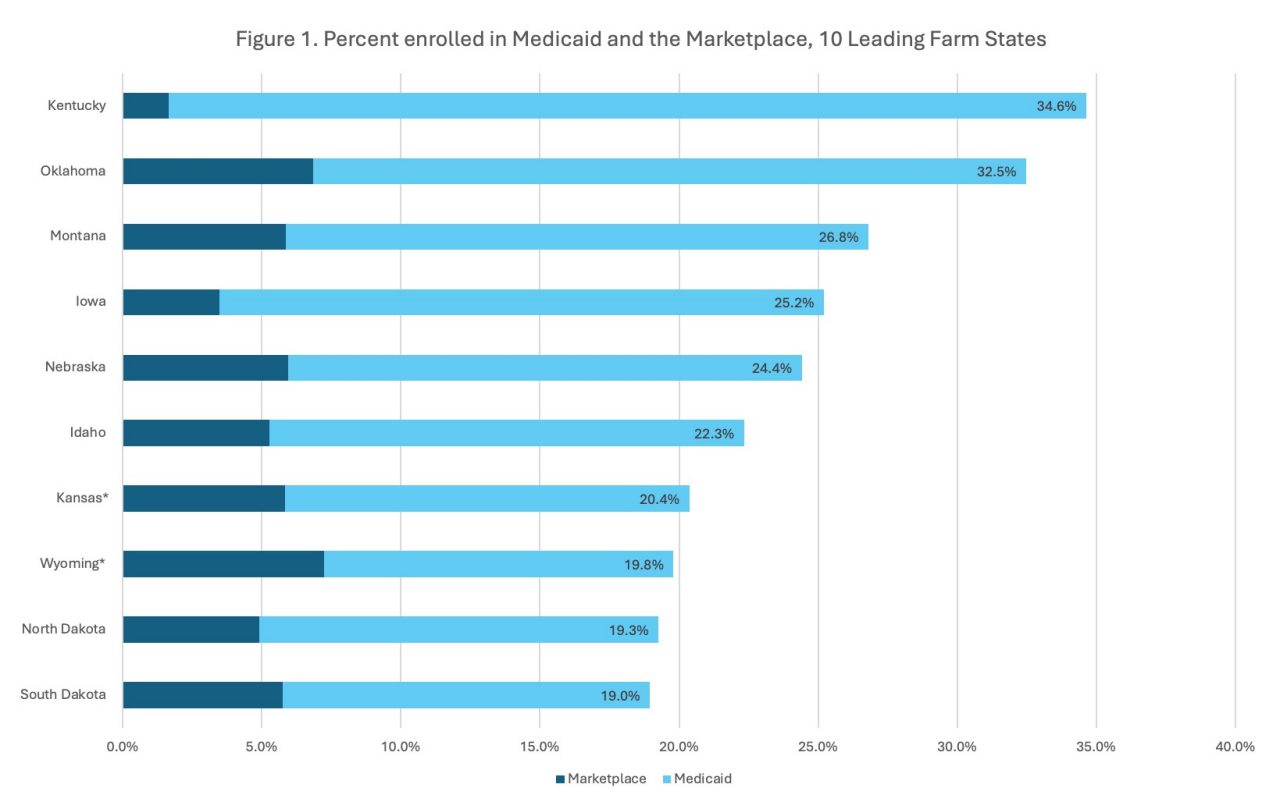

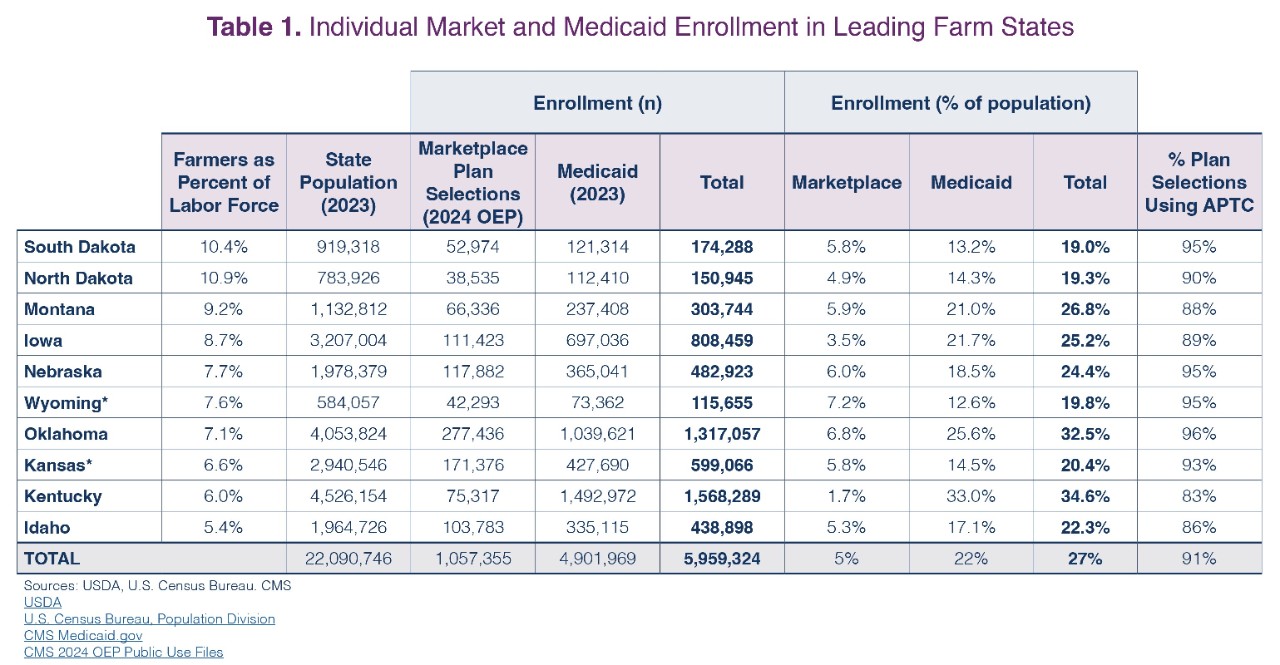

The individual market reforms and the expansion of Medicaid under the Affordable Care Act created new coverage options for farm families and rural residents, and the recent release of 2024 plan selection data provides a timely opportunity to examine the joint importance of the Marketplace and Medicaid in farm states. Table 1 shows the leading farm states, where the share of the labor force that farms ranges from 5.4% in Idaho to 10.4% in South Dakota. Nearly 6 million residents of these 10 states are enrolled in Medicaid or the Marketplace, more than one-quarter of their entire population. Approximately 1 million residents had selected plans in the Marketplace, and about 5 million residents were enrolled in Medicaid. As seen in Table 1 and Figure 1, the share of the total population enrolled in Medicaid and the Marketplace ranges from about one-fifth to one-third across states.

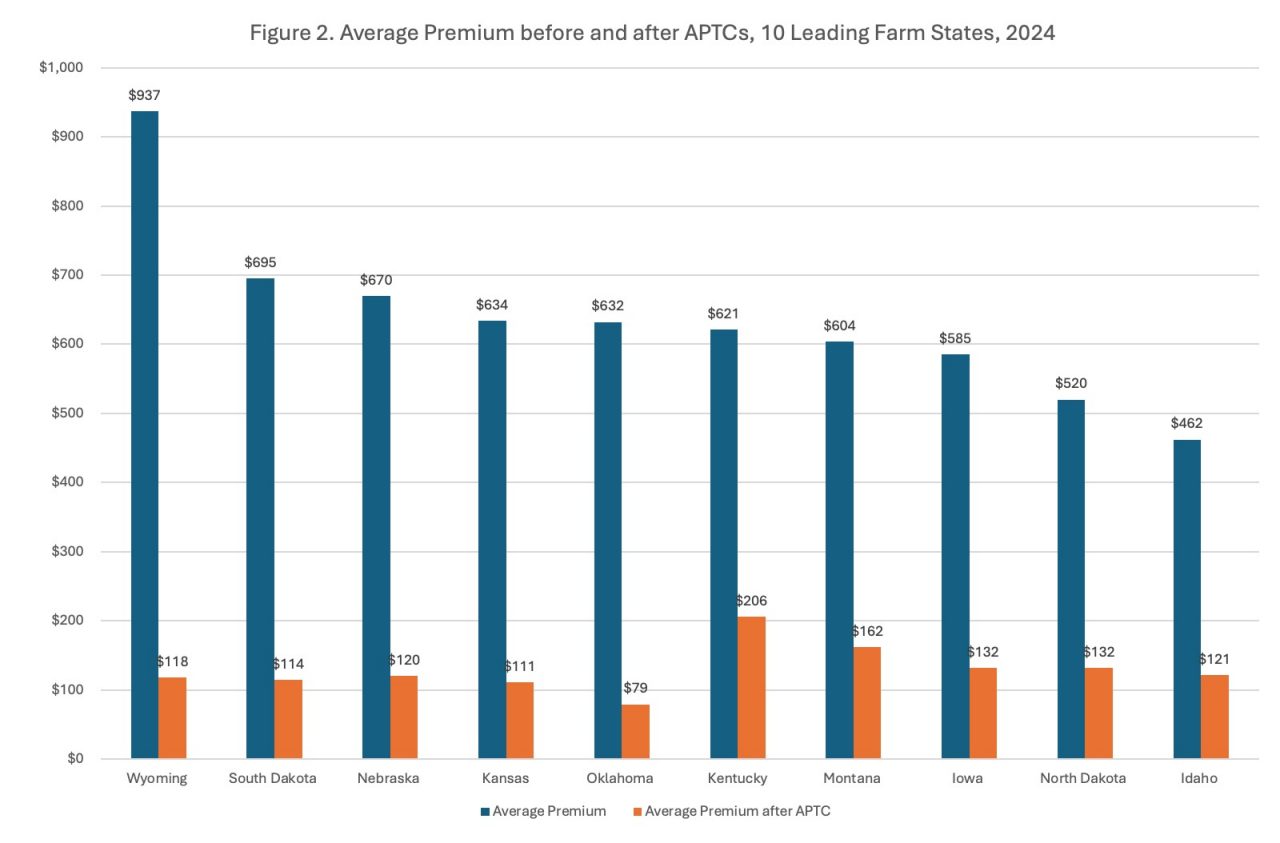

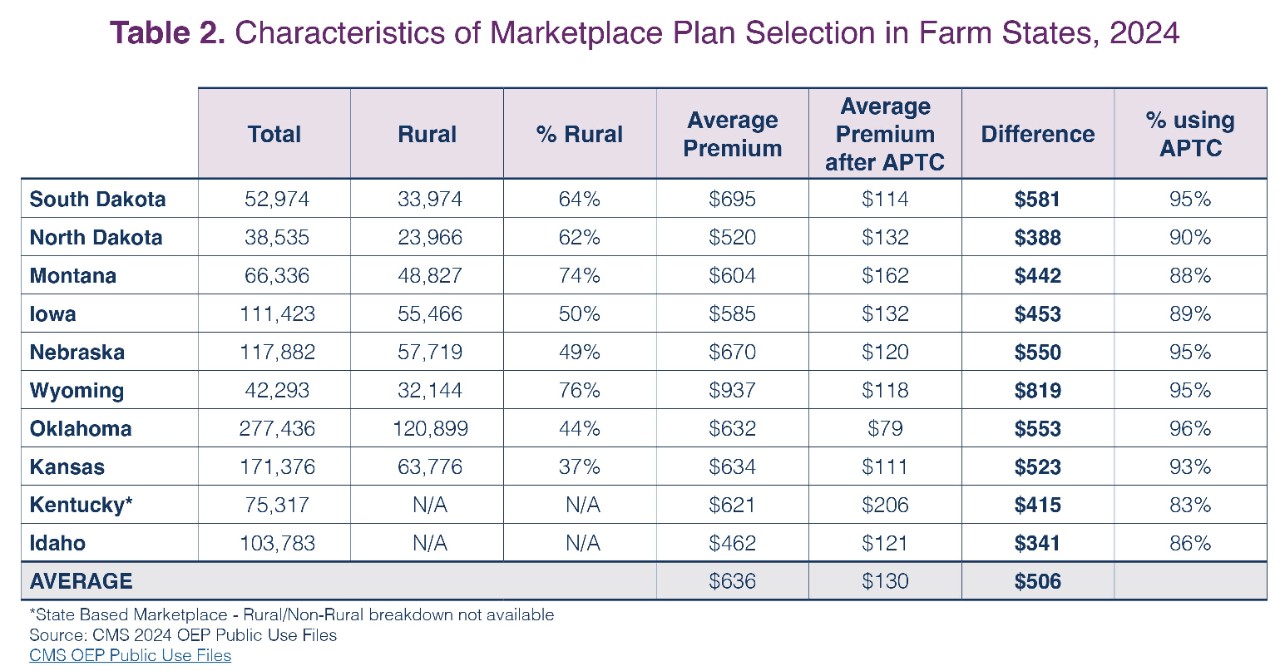

Table 2 provides some detail about enrollment in the Marketplace. The proportion of enrollees that are rural is generally high. In most states, more than half of those making plan selections are rural residents. In Wyoming and Montana, about three-fourths of residents that made plan selections were rural. Also notable is the very high use of the advance premium tax credits (APTCs) and the large impact they have on monthly premiums. Since these states are relatively rural, health insurance premiums are generally higher than the national average. In Wyoming, for example, average monthly premiums were $937 before the tax credit and $118 after the tax credit. Overall, the APTCs made a big difference in affordability, reducing monthly premiums by $506 on average across all ten states. Farmers earning more than 400% of the Federal Poverty Limit would receive no subsidy in the absence of the expanded APTCs and given the high cost of health insurance in rural states, many would face very high premium costs. The state differences in premiums resulting from the APTCs can be seen in Figure 2.

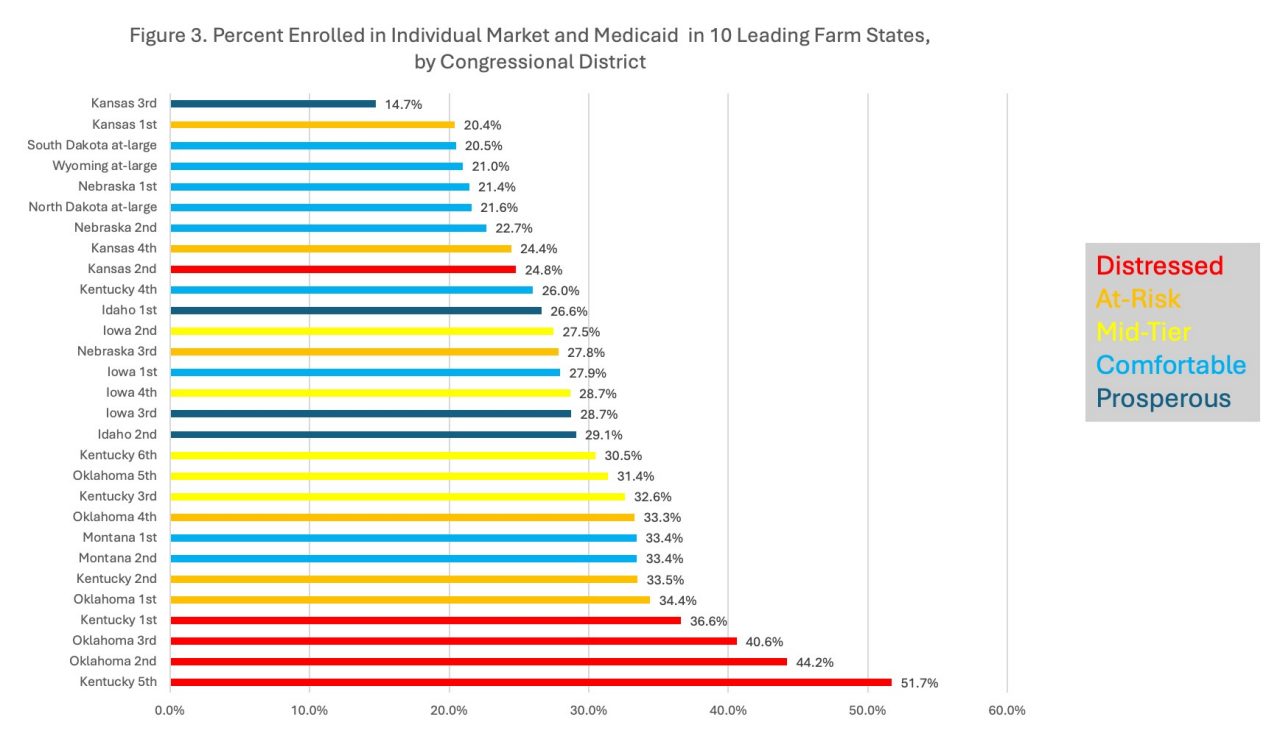

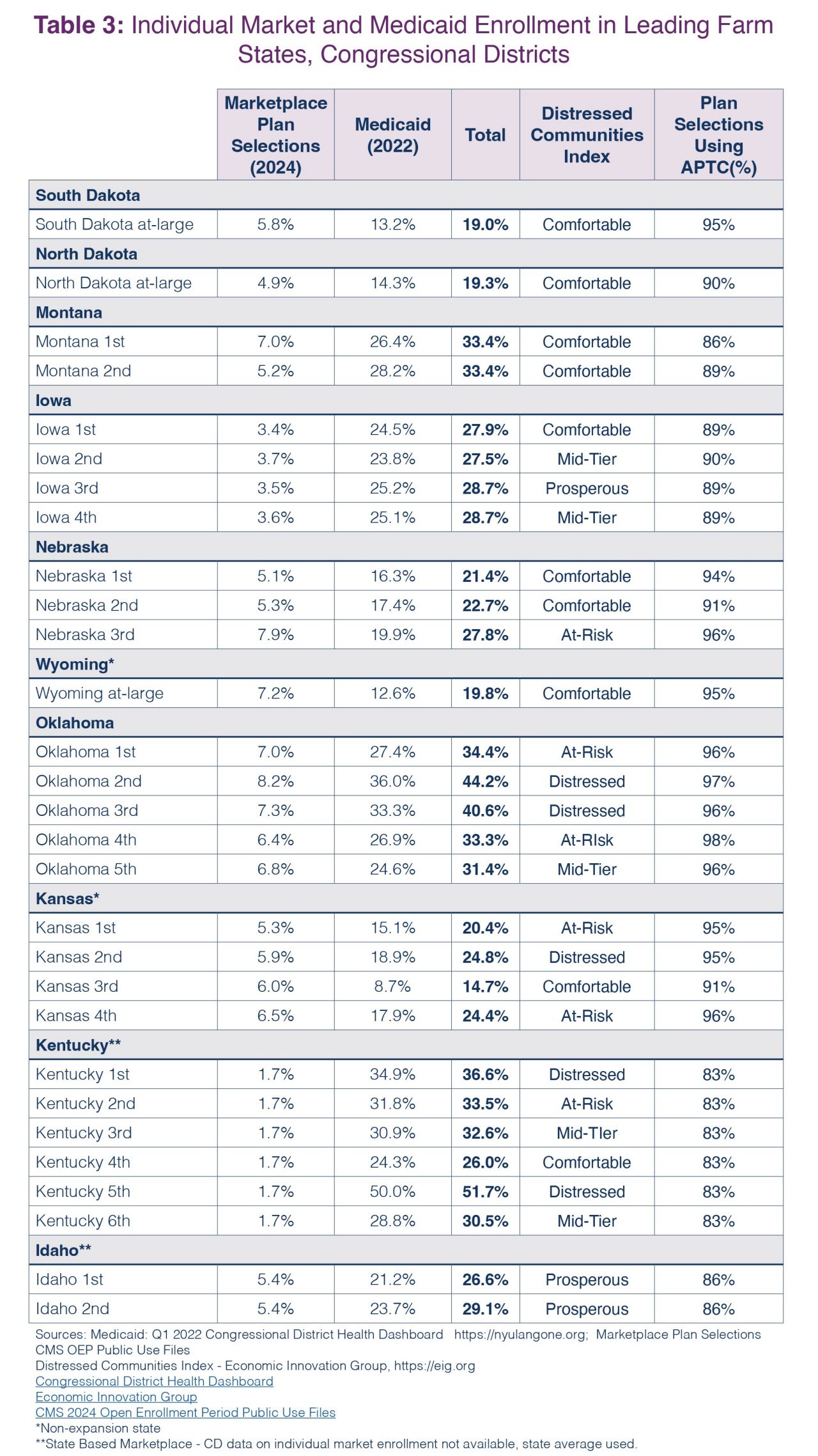

Table 3 shows enrollment in Medicaid and the Marketplace by congressional district for these 10 states. Due to their small populations, several of these states (South Dakota, North Dakota, and Wyoming) have only an at-large district, but the others have multiple districts, allowing for the observation of smaller area variation in program enrollment. For some congressional districts, such as in Kentucky and Oklahoma, about half of residents are participating in either Medicaid or the Marketplace. The lowest rate was seen in Kansas where, in one district, fewer than 15% of residents participated. It should be noted that Kansas and Wyoming have not yet expanded Medicaid, which almost certainly is depressing population enrollment in that program in those states. Kentucky and Idaho have State Based Marketplaces and do not participate in the Healthcare.gov platform, so congressional district level enrollment data were not available. For these two states, the state average was used for all congressional districts. Finally, the congressional districts were stratified by the Economic Innovation Group's Distressed Communities Index, a measure that divides communities into quintiles based on Census data on factors such as labor force participation, employment, education, housing, and income.

There are a few caveats that should be noted. The Marketplace data reports plan selections, which overstates to a small extent actual enrollment, since some people select a plan but then don't actually enroll. The most recent Medicaid enrollment data does not reflect the completion of the redetermination process, and may therefore somewhat overstate the population currently enrolled in Medicaid in these states. Total population is used, but this may understate the prevalence of these programs among those that are eligible, since the population over the age of 65 is generally ineligible for Marketplace coverage. These limitations are minor, but these estimates should be seen as a rough barometer of the importance of these programs to residents of these states rather than exact rates.

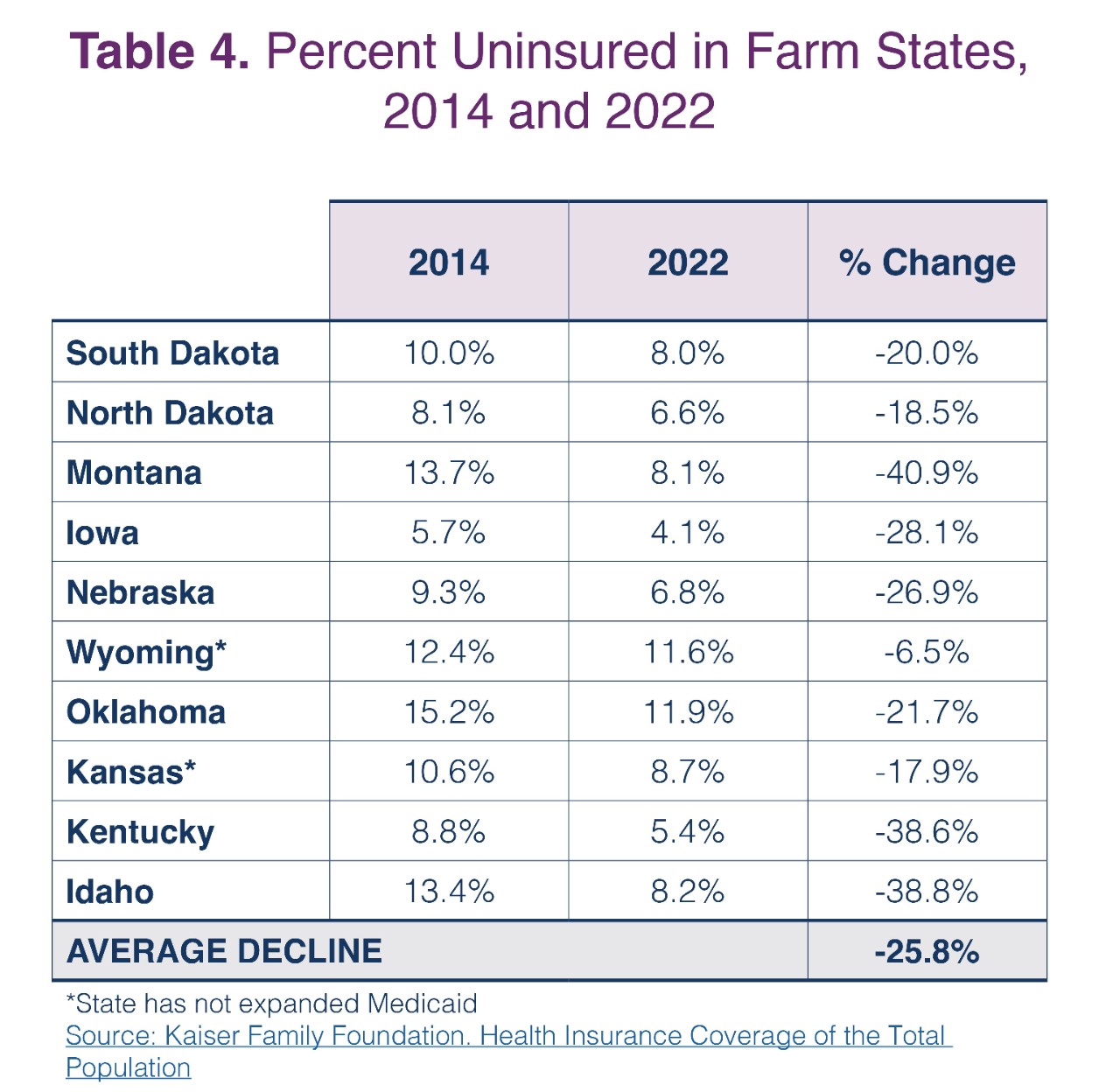

At a high level, the message is clear: Medicaid and the Marketplace are important sources of health insurance coverage in farm states for farmers and their families, rural residents, and others. For the population enrolled in the Marketplace, the use of the APTCs is nearly universal and these tax credits have a substantial impact on affordability—particularly in states like Wyoming where premiums are far above the national average. The population impact of these coverage options is reinforced by observing the downward trend in uninsurance rates since 2014, as shown in Table 4. All 10 states have seen a decline, with an approximately 40% drop in the percent uninsured in Montana, Idaho, and Kentucky. On average, the uninsured rate declined by about 25% for these ten leading farm states, a meaningful change in a very important indicator of health and financial wellbeing.

Related Content

Marketplace Pulse

Rural Health