Marketplace Pulse: Coverage of Obesity Therapies in State-Regulated Markets

The Marketplace Pulse series provides expert insights on timely policy topics related to the health insurance marketplaces. The series, authored by RWJF Senior Policy Adviser Katherine Hempstead, analyzes changes in the individual market; shifting carrier trends; nationwide insurance data; and more to help states, researchers, and policymakers better understand the pulse of the marketplace.

As demand for new weight loss medications grows, there is increased focus on the insurance coverage landscape. Due to the high cost of GLP-1s and the need for continued treatment, insurance coverage is essential for most patients, but unfortunately coverage policies are complex, highly variable, and frequently changing, creating a frustrating and confusing environment for patients and providers. For example, North Carolina recently ended coverage for state employees, while Michigan Blue Cross Blue Shield (BCBS) announced major changes in coverage for employer plans. An additional barrier is that plans that cover GLP-1s generally use some type of prior authorization process to limit patient access. This may include restrictions based on patient Body Mass Index (BMI) and prior weight loss attempts, as well as limitations on the length and quantity of medications prescribed. These conditions vary significantly among plans and insurance segments and are changing quickly as insurers develop new theories about how best to manage use of these new therapies. Out of pocket costs for patients also vary, since formulary tier placement and cost-sharing for prescription drugs are not uniform.

Given the high demand and the complex and rapidly changing coverage environment, patients, providers, advocates, and policymakers are seeking better information about the insurance coverage landscape. In response, RWJF recently sponsored a new source of data, the Obesity Coverage Nexus. This publicly available tool provides data about the insurance coverage of obesity treatments by state, including bariatric surgery and GLP-1 medications for most types of insurance coverage. (In addition to this publicly available resource, there is an opportunity to apply for a license to access more granular data at no-cost for non-commercial use.)

Coverage of GLP-1 medications varies significantly by health insurance segment. Notably, these drugs are currently not covered for weight loss in Medicare, due to a long-time exclusion of treatment for weight loss. However, Wegovy is covered in Medicare for other indications such as cardiac disease. There are ongoing efforts to reverse the Medicare ban on obesity treatments, including advocacy in favor of the Treat and Reduce Obesity Act of 2023 (TROA), a scaled-back version of which recently passed out of the House Ways and Means Committee. The estimated cost of adding this coverage has complicated the issue.

The employer segment, where approximately 160 million people receive coverage, is the site of the most visible turmoil, with frequent public announcements of changes in insurer policy. The self-insured part of the employer market is more likely to cover GLP-1s, since employers may feel pressure to cover the medications, and because the tenure of workers is generally longer in larger self-insured companies. This distinction was evident when the Michigan BCBS recently announced some changes to their coverage of GLP-1 medications.. In the self-insured market, the company changed the prior authorization requirements to require that patients participate in a weight loss program and also required that patients have an in-person relationship with their prescriber. For the fully insured market, BCBS Michigan will end coverage of GLP-1 medications completely beginning on renewal or January 2025, whichever is first. The company cited its own research, noting that it showed that "most patients aren't staying on GLP-1 drugs for weight loss long enough to see a benefit."

Compared to the employer market, the individual market is known for relatively restrictive coverage in terms of provider networks and cost-sharing for prescription drugs. It also has a structure where individuals shop for plans and can view prescription drug formularies to help make decisions about which plan to choose. This has previously led to an issue with HIV medications, where, concerned about the potential for selection, all insurers offering plans in certain rating areas placed all HIV medications in the highest formulary tier. After a successful advocacy effort, this practice was recognized as discriminatory and plans were forbidden from doing this. But in a context where coverage of GLP-1s is not required, (although in a recent column it was proposed that anti-obesity medications should be considered preventive by the US Preventive Services Task Force) an insurer might fear adverse selection if they covered the medications while their competitors did not. Even though risk adjustment is ostensibly designed to remove concerns about selection, it does not function perfectly, overpaying for some risks while underpaying for others. The relationship between GLP-1 use and overall experience is not yet generally understood and is changing as the coverage environment evolves. Insurers generally seek to avoid changes in risk that they don't understand. Finally, the generally short-term nature of the enrollee-insurer relationship in the individual market would be expected to deter most insurers from adopting a "long run" view about potential benefits of GLP-1s that might exceed short-term costs.

All this is to say that we would expect the prevalence of coverage of GLP-1s in the individual market to be quite low compared to the self-insured employer market. Reflecting this, a recent assessment of the states that use the federally facilitated marketplace (Healthcare.gov) found that fewer than 1% of plans covered Wegovy for weight loss. Here we broaden the scope to include states with their own exchanges. We also examine coverage in other state regulated insurance markets: the small group market, state employee plans, and Medicaid to see whether there is evidence of emerging regional patterns in coverage of GLP-1s.

Individual market

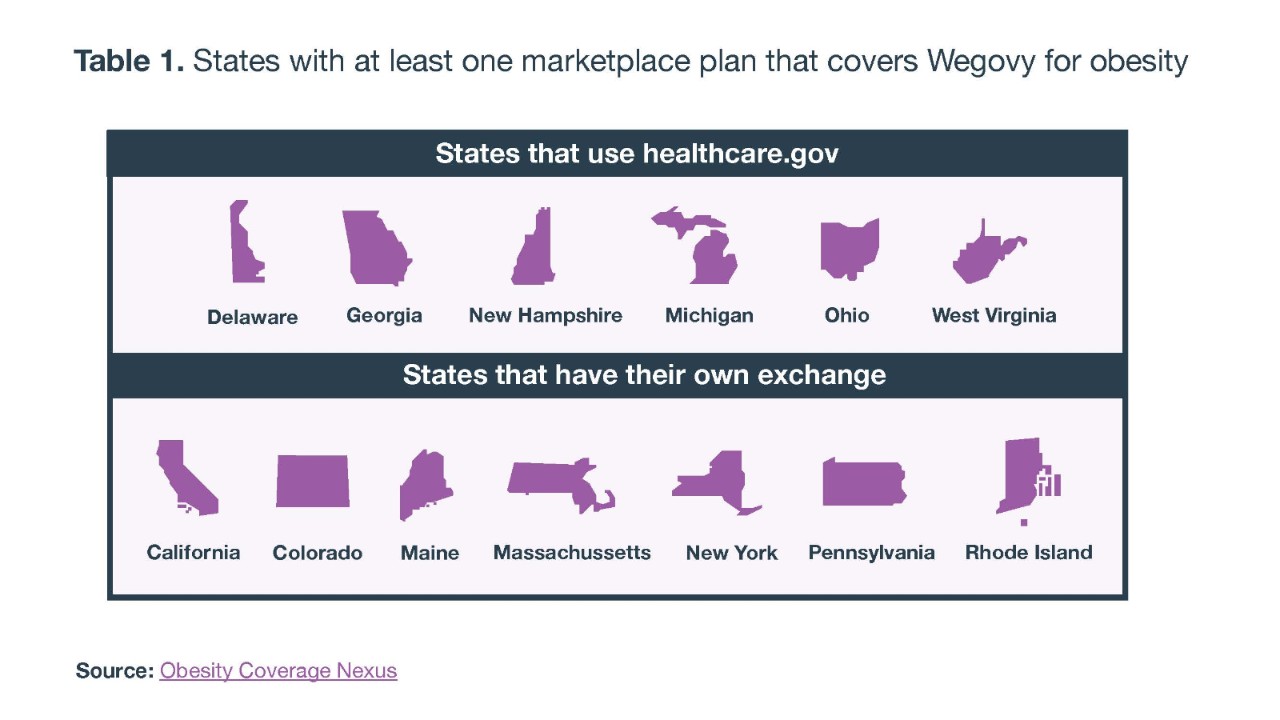

Table 1 shows the 13 states where at least one marketplace plan covers Wegovy for obesity. Overall, the prevalence of coverage in the individual market is very low but not nonexistent and is more prevalent in states that have their own insurance exchange. There are six states with coverage that use the Federally Facilitated Marketplace (FFM) (Healthcare.gov) and seven that have their own state-based marketplaces (SBM). Yet among the SBM states, several of the states (NY, CA, and MA) have more than one plan that covers Wegovy for obesity, and the estimated individuals enrolled in plans with coverage is nearly 800,000 in the SBM states, versus only about 70,000 in the plans that cover Wegovy in the FFM. It is worth noting that many of the states with coverage are in the New England and mid-Atlantic region. With the exception of California, all of the SBM states are from those regions, as are two of the FFM states (DE and NH). Overall, however, the picture is one of very low coverage. There are fewer than 1 million enrolled individuals in plans with coverage, less than 5% of total Marketplace enrollment.

Other state regulated markets

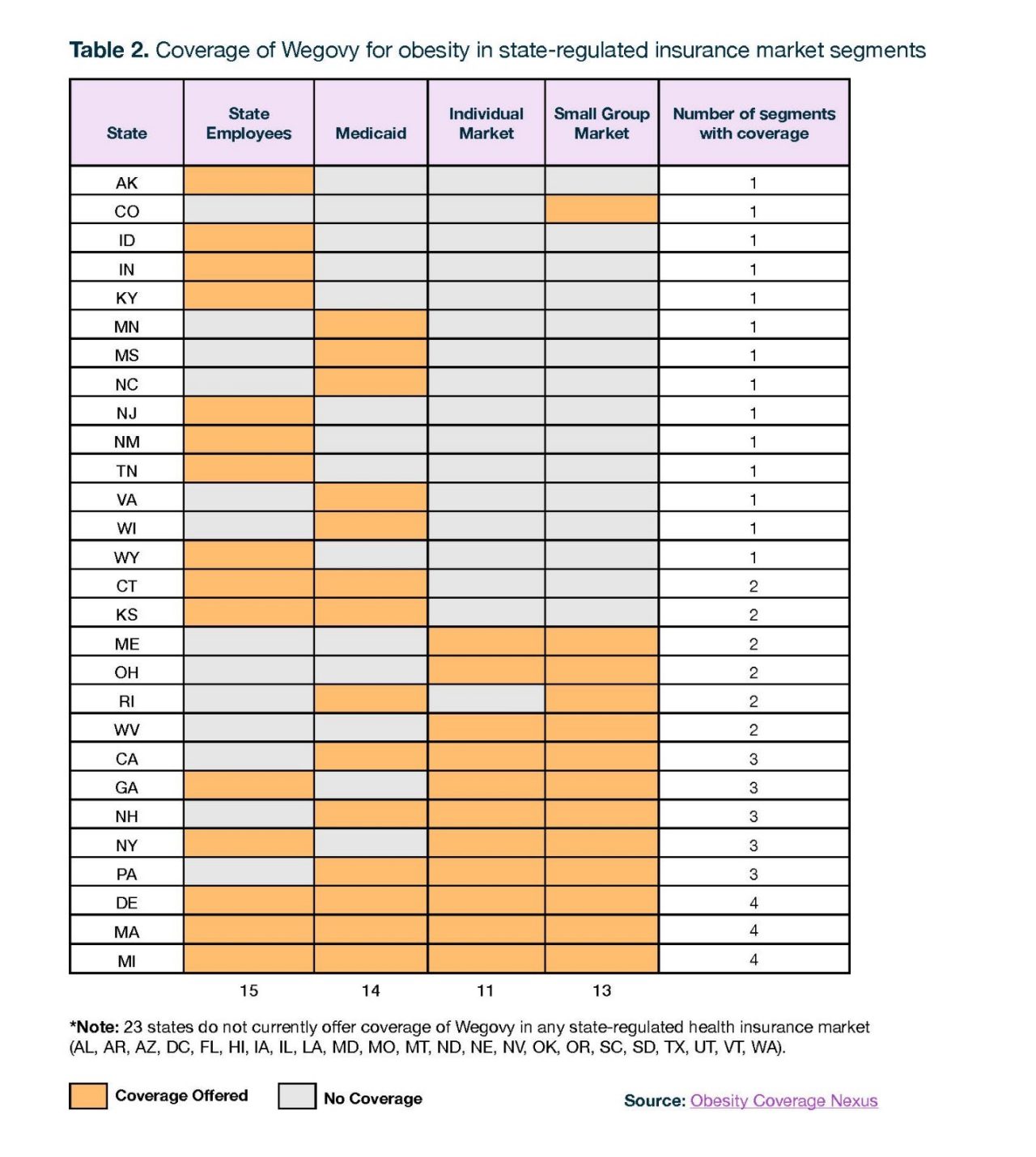

Table 2 shows the status of coverage of Wegovy for obesity in four state-regulated health insurance markets: Medicaid, state-employee plans, the small group market, and the individual market. In general, if a drug is covered in Medicaid or the state employee plans, it will be available to all enrollees. For the small group and individual market there may be coverage by some insurers but not others meaning that the percentage of enrollees in that segment that have access to the drug may not be particularly high. For simplicity, Table 2 shows whether there is ANY coverage of Wegovy for obesity in these market segments. The likelihood of coverage does not differ much between these segments. For example, 15 states cover Wegovy for obesity in the state employee plan, while 14 states cover it in Medicaid. Wegovy is covered for obesity in the small group and individual market in 11 and 12 states, respectively.

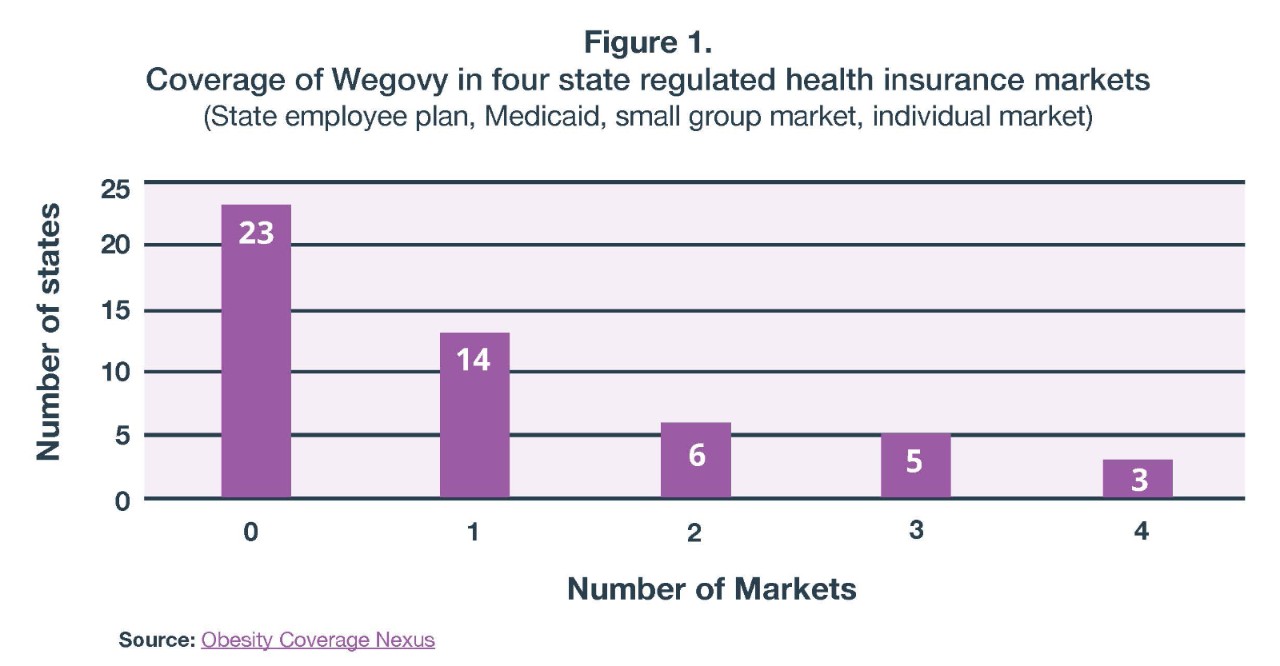

As can be seen in Figure 1, in nearly half of states there is no coverage of Wegovy for obesity in any of these four health insurance markets. In 12 states there is coverage in one market, six states have coverage in two markets, five states have coverage in three markets, and in just three states there is coverage in all four markets. Again, coverage in the small group and individual markets signifies that at least one plan covers Wegovy in these markets, which could translate into a very low percentage of enrollees that are actually in a plan with coverage.

There is an emerging regional pattern, with Southern and Western states having the least coverage and Northeastern and Midwestern states having the most. California is the sole western state where there is some coverage of these plans. In the South, some exceptions are Kentucky, Georgia, and Tennessee, which cover Wegovy for state employees, and Mississippi and North Carolina, which provides coverage in Medicaid. Georgia also has some coverage in the small and individual market. With high unmet demand for GLP-1 medications and concerns about cost and adherence, there will be continued interest in monitoring insurance coverage policies in state regulated markets.

This variable pattern of state coverage decisions also raises important health equity issues. The geography of coverage amplifies an ongoing problem with racial difference in access, with studies showing Black people to be less likely to receive prescriptions for GLP-1s, despite being more likely to be affected by obesity. These differences are attributable to factors stemming from historic racial discrimination, including differences in insurance coverage and income, since for those who do not have coverage, the retail cost of these medications is roughly $1,000 per month. Black people are disproportionately likely to live in Southern states, which as a region has a higher prevalence of obesity and lower income when compared to the rest of the country. Yet as these data show, Southern residents are less likely than others to have access to GLP-1 drugs in state regulated health insurance markets, providing another example of how state of residence can affect access to healthcare in critical ways.

Related Content